As an example, if a property has a worth of $200,000 and the insurance supplier needs an 80% coinsurance, the owner must have $160,000 of home insurance coverage. Owners may include a waiver of coinsurance clause in policies. A waiver of coinsurance provision relinquishes the homeowner's requirement to pay coinsurance.

In some cases, however, policies may consist of a waiver of coinsurance in the occasion of a total loss. Coinsurance is the amount a guaranteed need to pay against a health insurance claim after their deductible is pleased. Coinsurance likewise uses to the level of home insurance coverage that an owner should buy on a structure for the coverage of claims.

Both copay and coinsurance arrangements are methods for insurance provider to spread danger among individuals it guarantees. Nevertheless, both have advantages and drawbacks for consumers.

Lots of or all of the items featured here are from our partners who compensate us. This may affect which products we discuss and where and how the product appears on a page. However, this does not influence our evaluations. Our viewpoints are our own. Medical insurance is unlike any other insurance coverage you buy: Even after you pay premiums, there are complex out-of-pocket costs like deductibles, copays and coinsurance.

It is essential to understand the fundamentals of medical insurance so you can make the ideal monetary decisions for your household prior to you need care. what is the fine for not having health insurance. That method, you can focus more on recovery when the time comes. Here's our guide on how the expenses of health insurance work. Before you comprehend how it all collaborate, let's brush up on some common medical insurance terms.

Like a health club membership, you pay the premium each month, even if you do not utilize it, or else lose coverage. If you're lucky sufficient to have employer-provided insurance coverage, the business generally chooses up part of the premium. A fixed rate you pay for healthcare services at the time of care.

The deductible is just how much you pay before your health insurance coverage begins to cover a bigger part of your expenses. In general, if you have a $1,000 deductible, you should pay $1,000 for your own care out-of-pocket prior to your insurance provider starts covering a higher portion of expenses. The deductible resets annual.

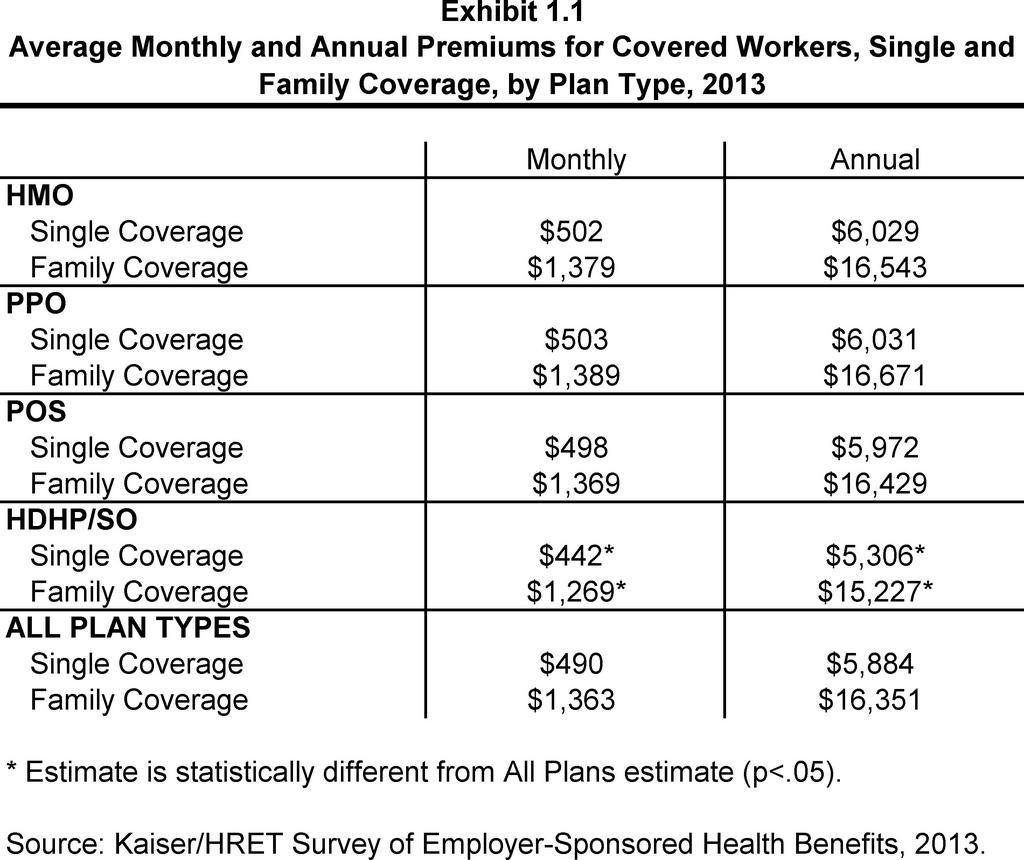

Fascination About How Much Is Private Mortgage Insurance

For example, if you have a 20% coinsurance, you pay 20% of each medical bill, and your medical insurance will cover 80%. The most you could need to pay in one year, out of pocket, for your health care prior to your insurance covers 100% of the expense. Here you can see the maximums permitted by the federal government for private prepare for this year.

Some policies have low premiums and high deductibles and out-of-pocket maximum limits, while others have high regular monthly rates and lower deductibles and out-of-pocket limitations. In general, it works like this: You pay a regular monthly premium simply to have medical insurance (how does health insurance deductible work). When you go to the medical professional or the medical facility, you pay either complete cost for the services, or copays as outlined in your policy.

The staying percentage that you pay is called coinsurance. You'll continue to pay copays or coinsurance until you have actually reached the out-of-pocket maximum for your policy. At that time, your insurance provider will begin paying 100% of your medical costs until the policy year ends or you switch insurance coverage strategies, whichever is initially.

If you utilize an out-of-network medical professional, you could be on the hook for the entire expense, depending on which type of policy you have. This brings us to three brand-new, associated meanings to understand: The group of medical professionals and companies who accept accept your medical insurance. Health insurance providers negotiate lower rates for care with the physicians, health centers and centers that remain in their networks.

If you get care from an out-of-network company, you might have to pay the entire bill yourself, or just a part, as shown in your insurance policy summary. A service provider who has actually consented to work with your insurance coverage plan. When you go in-network, your bills will normally be less expensive, and the expenses will count toward your deductible and out-of-pocket maximum.

Your expenses would be various based upon your policy, so you'll wish to do your own calculations each year when dealing with a medical cost. Vigilance is single and has an annual deductible of $1,200. Her insurance strategy has some copays, which do not count towards her deductible. After she meets the timeshare escape deductible, her insurance company pays 80% of her medical costs, leaving Prudence with coinsurance of 20%.

Due to the fact that she goes to an in-network supplier, this is a totally free preventive care visit. Nevertheless, based on her physical, her main care doctor thinks Prudence needs to see a neurologist, and the neurologist advises an MRI. Copays for an in-network professional on her plan are $50, which she should pay, while her insurer will cover the rest of the neurologist's charge.

The Facts About How Much Does Insurance Go Up After An Accident Revealed

Imaging scans like this are "based on deductible" under Vigilance's policy, so she must pay for it herself, or out-of-pocket, since she hasn't satisfied her deductible yet. So her insurance company won't pay anything to the MRI center. $50 for the neurologist copay + $1,000 for the scan = $1,050. Later on in the year, Vigilance falls while hiking and injures her wrist.

After the copay, ER charges were $3,400. Her deductible will be applied next. Prudence paid $1,000 of her $1,200 deductible previously in the year for her MRI, so she is accountable for $200 of the ER costs before her insurer pays a larger share. After deductible and copay, the ER charges total $3,200.

$ 100 for the ER copay + $200 for remaining deductible + 20% coinsurance ($ 640) = $940. Vigilance has actually now paid $1,990 towards her medical costs this year, not including premiums. She has actually also fulfilled her annual deductible, so if she requires care again, she'll pay only copays and 20% of her medical bills (coinsurance) up until she reaches the out-of-pocket optimum on her strategy.

Comprehending healthcare can be confusing. That's why it's valuable to understand the significance of frequently used terms such as copays, deductibles, and coinsurance. Knowing these important terms may assist you understand when and how much you need to spend for your healthcare. Let's take a look at the definitions for these three terms to much better understand what they Click here! suggest, how they collaborate, and how they are various.

For example, if you hurt your back and go see your doctor, or you need a refill of your kid's asthma medicine, the amount you spend for that check out or medicine is your copay. Your copay amount is printed right on your health strategy ID card. Copays cover your portion of the expense of a physician's visit or medication.

Not all strategies utilize copays to share in the cost of covered costs. Or, some strategies might utilize both copays and a deductible/coinsurance, depending on the type of covered service. Also, some services might be covered at no out-of-pocket expense to you, such as yearly examinations and getting rid of timeshare maintenance fees certain other preventive care services. * A is the quantity you pay each year for most eligible medical services or medications prior to your health strategy starts to share in the cost of covered services. how to get a breast pump through insurance.